Suze Orman is Wrong About IBC® and Dividend-Paying Whole Life Insurance: The Institutional Evidence

Suze's statements on permanent life insurance come from a place of either knowledge deficit or intentional misdirection.

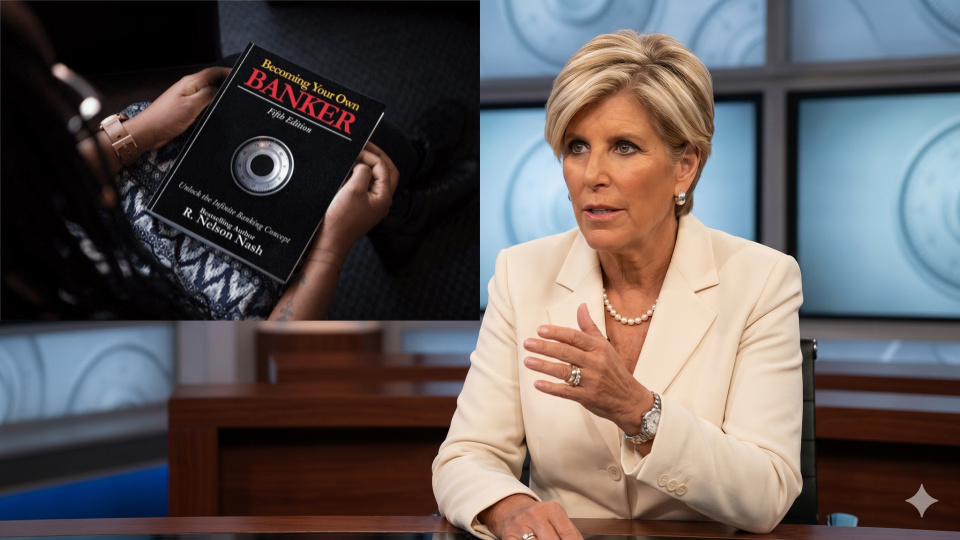

When you begin evaluating the Infinite Banking Concept (IBC®) and the logic of Becoming Your Own Banker®, you will inevitably hit a wall of mainstream financial dogma.

This week, during a discussion with a woman about using dividend-paying whole life insurance as a liquid, guaranteed capital asset, she brought up a common objection: “Suze Orman says whole life is too expensive and a bad financial move. She says you should only buy term life insurance and invest the difference.”

In person, it is relatively simple for me to demonstrate how these statements are fallacious, rigid, and entirely ignore the macroeconomics of corporate wealth. But to truly understand why media personalities push these narratives, we have to look behind the curtain of network television.

This isn't just my perspective. To uncover the truth, we have to look at credible research that the average person claiming to be "financially literate" has never even heard of.

Media Madness and Truth Decay

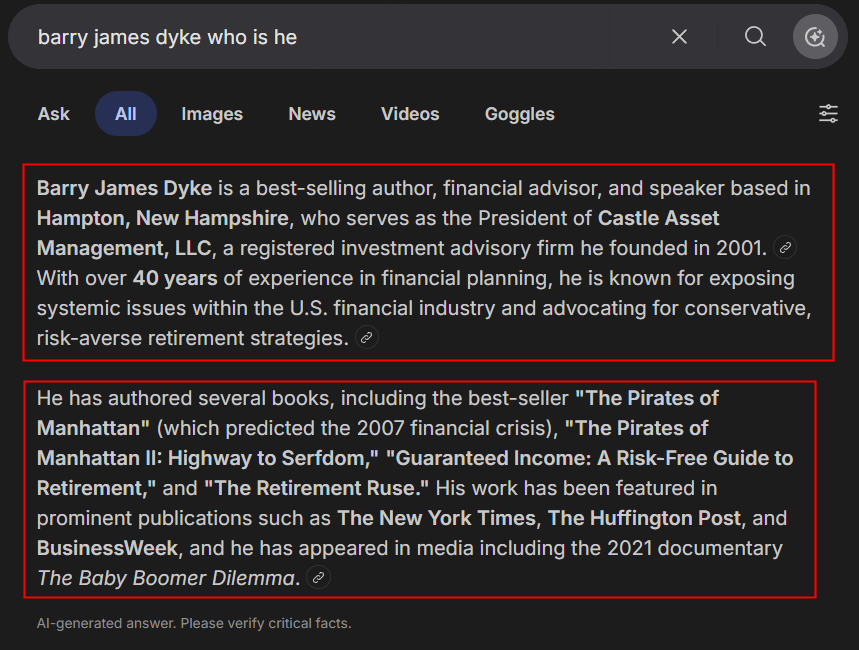

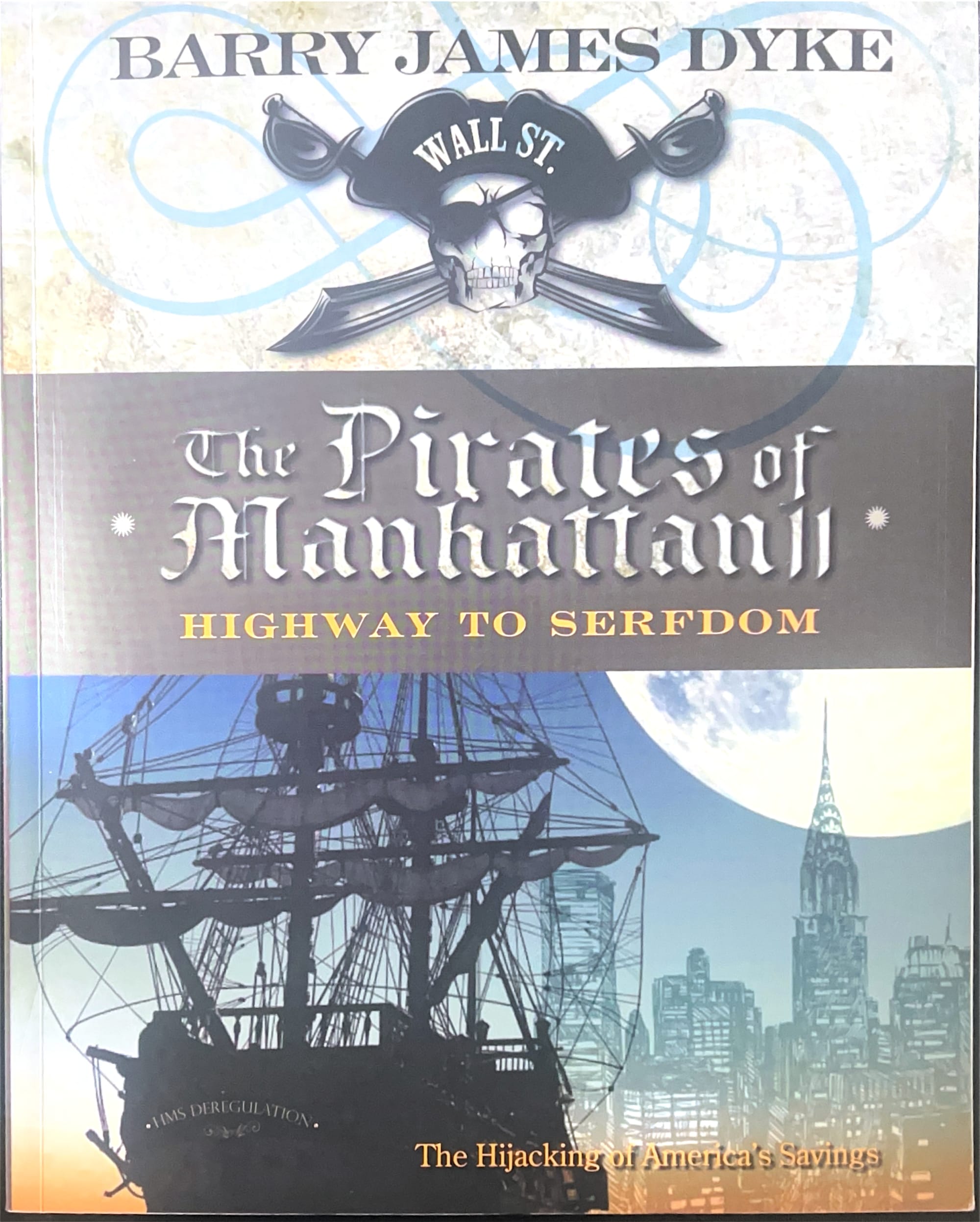

In my private library, I keep a collection of research books focused on actual institutional financial architecture. One of those hidden gems is Pirates of Manhattan II: Highway to Serfdom (2012) by distinguished financial professional and author Barry James Dyke.

In Chapter 3, titled "Media Madness and Truth Decay," Dyke dedicates a comprehensive section (pp. 146–153) to exposing exactly how financial institutions use media celebrities to promote Wall Street’s agenda. He explicitly names the figures used to direct public behavior: Peter Lynch, Jane Bryant Quinn, Dave Ramsey, and Suze Orman.

Dyke reveals a profound, undeniable double standard: The mass-media financial entertainers tell everyday Americans to take 100% of the market risk in volatile retail products, while the corporations funding those media networks, do the exact opposite with their own capital.

The Corporate Double Standard: What the SEC Filings Reveal

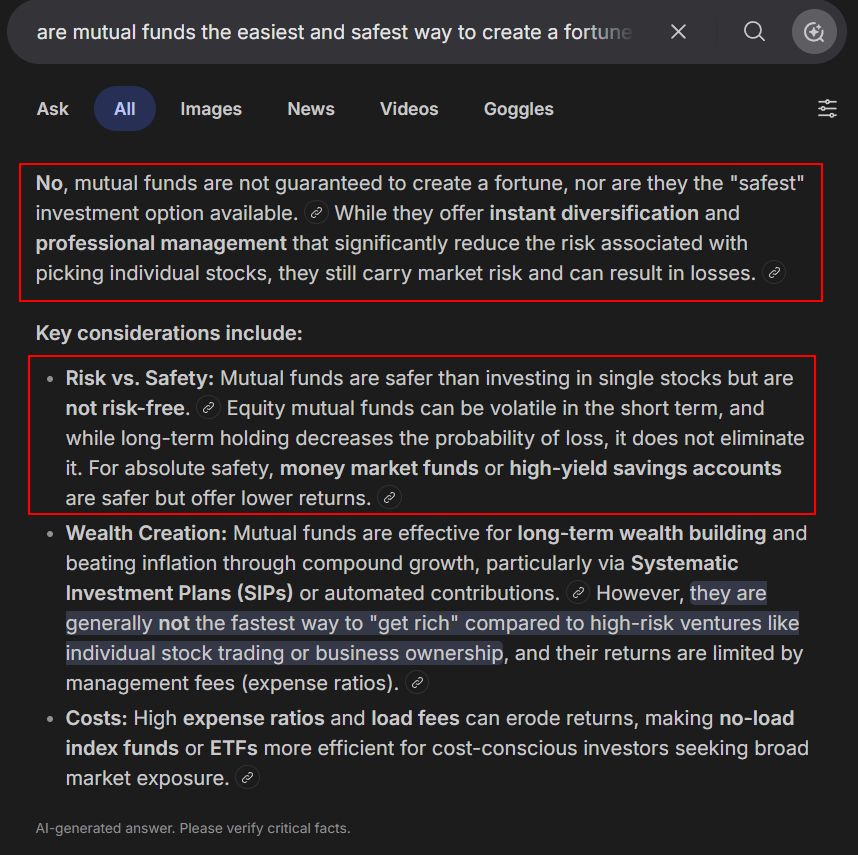

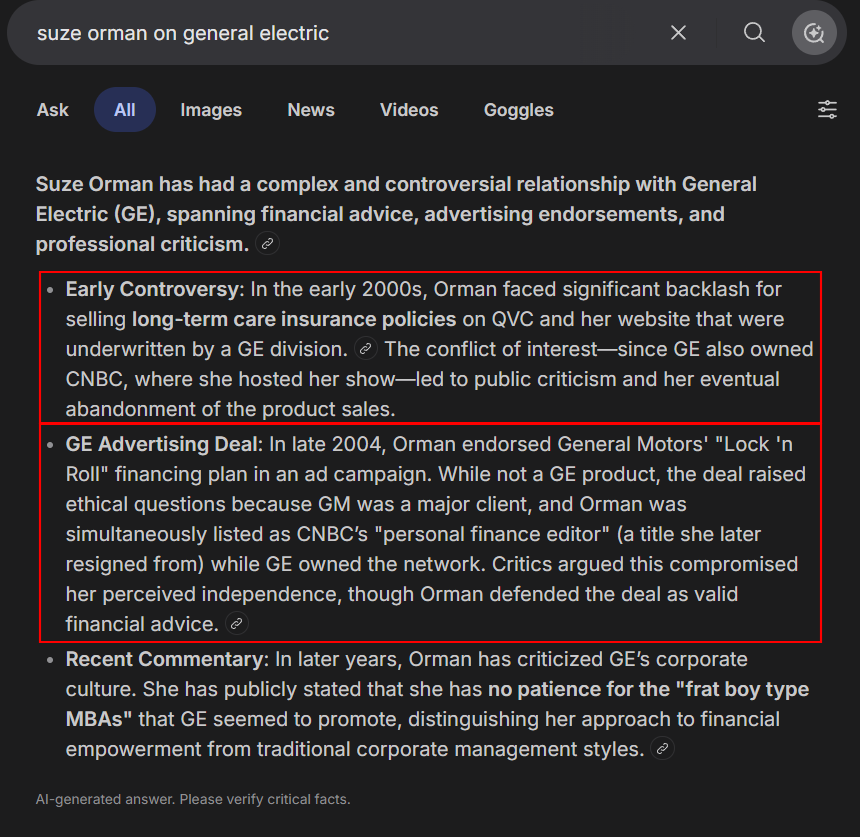

Suze Orman has historically demonized whole life insurance while publicly stating that mutual funds are the easiest and safest way to build wealth.

Yet, an analysis of the corporate networks she is affiliated with—such as CNBC, Comcast, and TD Ameritrade—reveals a massive conflict of interest.

Consider General Electric (GE), a massive corporate syndicate tightly woven into this media ecosystem. While mainstream television programming instructs the working class to buy temporary term insurance and dump their savings into 401(k)s and mutual funds, the executives at the top are quietly anchoring their wealth in permanent, cash-value whole life insurance.

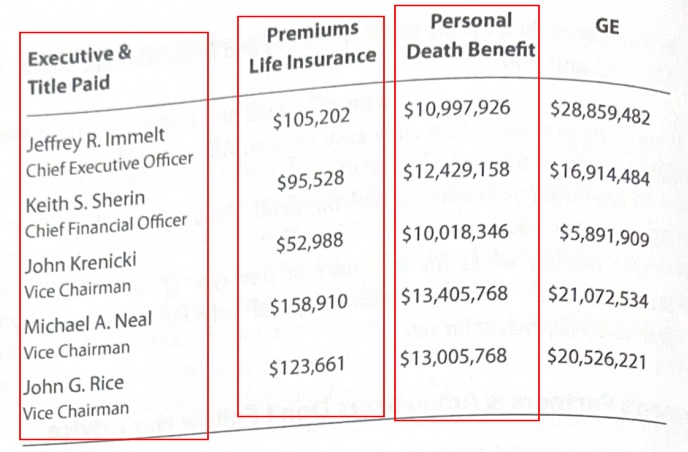

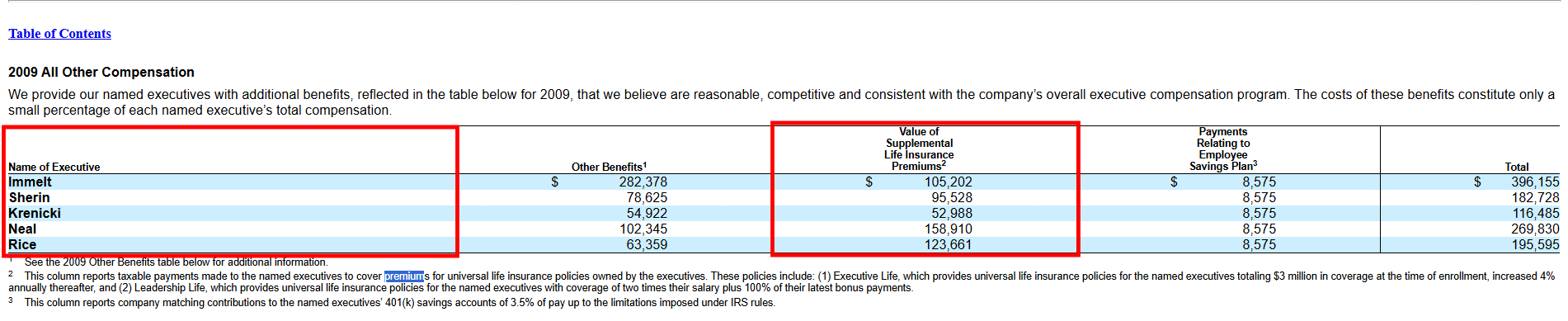

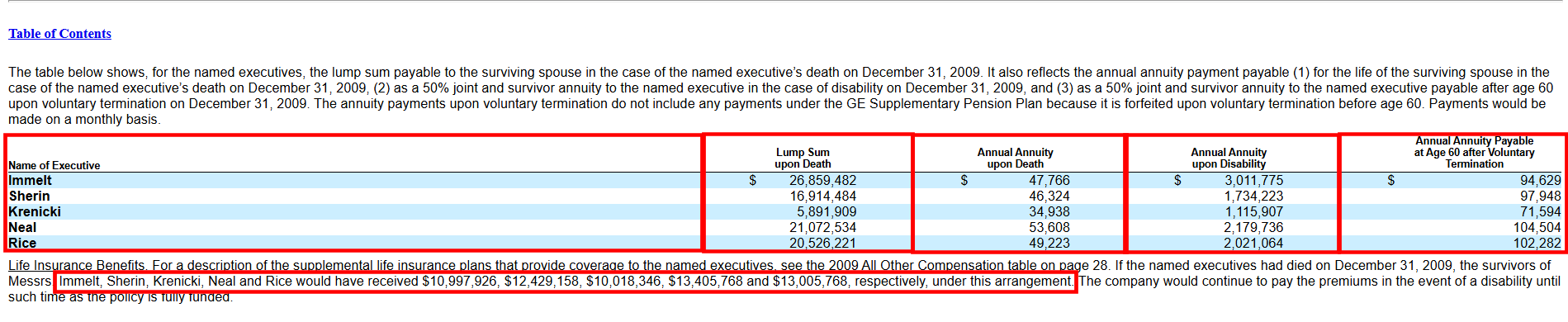

This isn't speculation; it is public record. Barry James Dyke highlights the General Electric SEC Proxy Filings (such as the 12/31/2009 disclosures).

When you examine the executive compensation tables and deferred compensation structures of the financial elite, you see millions upon millions of corporate dollars flowing directly into permanent life insurance assets owned by the executives and the banks themselves.

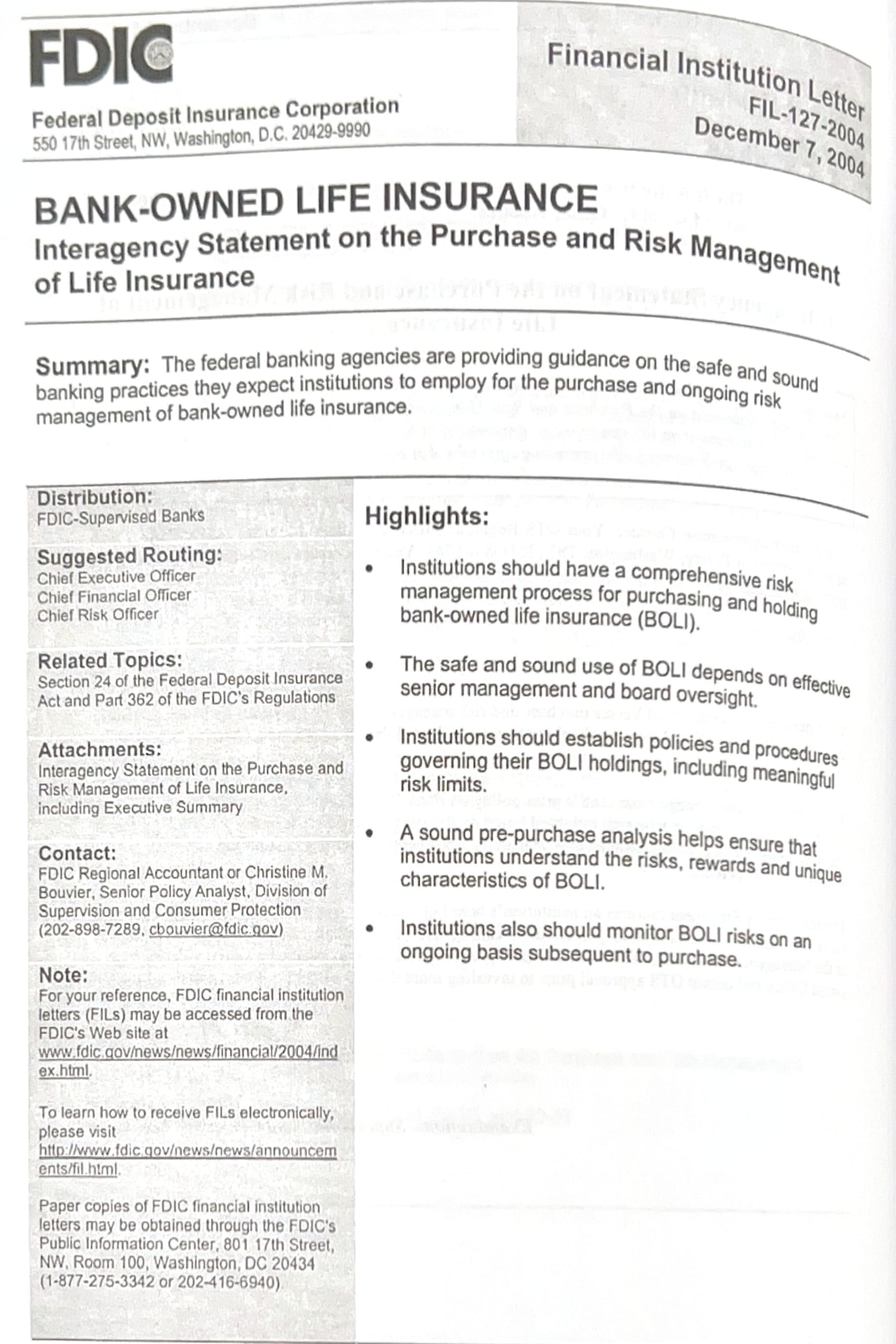

The same reality applies to commercial banking institutions and even the FDIC. They maintain massive allocations of Tier-1 capital in Bank-Owned Life Insurance (BOLI) because they require guaranteed growth, tax insulation, and immediate liquidity to operate.

- The Public Mandate: Buy a term policy that statistically has a 99% failure rate of ever paying out a claim, and invest your liquid savings into volatile, fee-heavy equity markets.

- The Institutional Mandate: Protect corporate reserves using the ironclad, contractual guarantees of dividend-paying permanent life insurance.

Knowledge Deficit or Intentional Misdirection?

The contradiction goes even deeper. It has been well-documented that the vast majority of Suze Orman’s personal multi-million dollar net worth is not even held in the retail mutual funds she peddles to the public.

This leaves the everyday saver with a stark logical conclusion. When a media personality uses a massive corporate platform to demonize an asset class that the corporate executives, commercial banks, and financial elites use to anchor their own wealth, it means one of two things:

- Either the "financial guru" completely lacks an understanding of institutional capital design and asset architecture.

- Or the "financial guru" is intentionally misinforming the general public to keep consumer liquidity flowing directly into the traditional commercial banking and Wall Street pipeline.

True financial equity requires moving past celebrity talking points and learning to model our personal capital structures after what the institutions do, not what their paid commentators say.

Read from Chapter 3 of Pirates of Manhattan II

To give you the opportunity to review the documentation and draw your own conclusions, I have uploaded the explicit pages from Barry James Dyke's text directly to this post.

Barry James Dyke’s Books & Official Site

For those interested in getting a full copy of Barry James Dyke's work, check out his website.